2026 Housing Market: Mortgage Rates, Affordability, and Future Trends

The housing market is a dynamic and often unpredictable beast, constantly influenced by a myriad of economic, social, and political factors. As we cast our gaze forward to the 2026 housing market, prospective homeowners, current owners, and investors alike are eager to understand what the future holds. Will mortgage rates continue their rollercoaster ride? Will affordability remain a persistent challenge, or will we see some relief? This comprehensive analysis delves into the anticipated trends, potential pitfalls, and opportunities that could define the real estate landscape in 2026.

Understanding the Current Landscape: A Precursor to the 2026 Housing Market

Before we can accurately predict the 2026 housing market, it’s crucial to understand the forces that have shaped the market in recent years. The post-pandemic era witnessed an unprecedented surge in demand, fueled by low interest rates, a desire for more space, and a shift towards remote work. This led to rapid price appreciation and intense competition, making homeownership a distant dream for many.

However, the latter half of 2022 and much of 2023 saw a significant shift. Aggressive interest rate hikes by central banks, aimed at taming inflation, sent mortgage rates soaring. This cooled demand, leading to a slowdown in price growth and, in some areas, modest price corrections. Inventory levels, while still historically low, began to tick up slightly. The market has been characterized by a delicate balance between persistent buyer demand and the increasing cost of borrowing, creating a complex environment for all stakeholders.

Several key indicators are currently under scrutiny: inflation rates, employment figures, consumer confidence, and global economic stability. These elements act as dominoes, each capable of influencing the others and, ultimately, the trajectory of the housing market. A strong labor market, for instance, can bolster demand, while stubbornly high inflation can pressure central banks to maintain higher interest rates. Understanding these interconnected variables is the first step in deciphering the puzzle of the 2026 housing market.

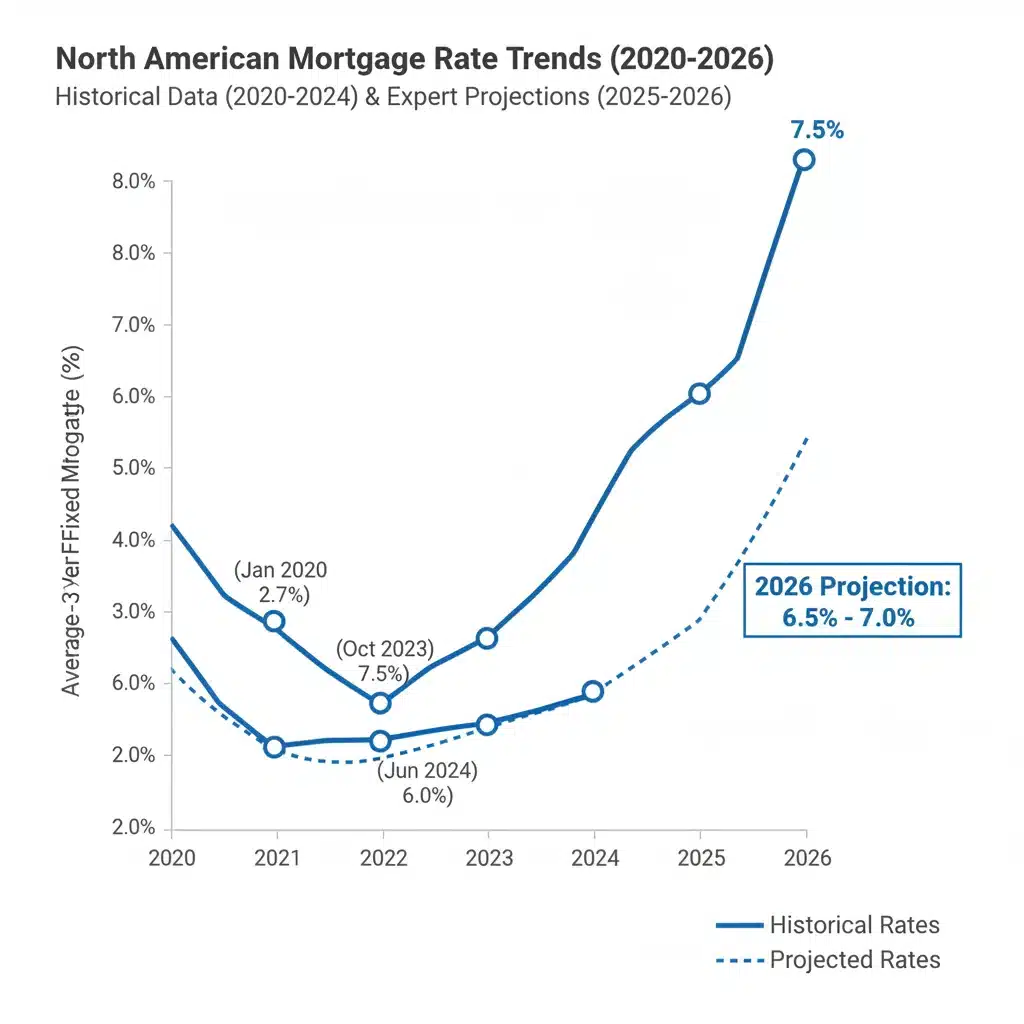

Mortgage Rate Trends: What to Expect in 2026

One of the most critical factors influencing the accessibility and affordability of housing is the movement of mortgage rates. Predicting these rates accurately for 2026 requires a deep dive into monetary policy, economic growth, and inflation expectations. While no one has a crystal ball, we can analyze prevailing economic theories and expert consensus to form a reasonable outlook.

The Federal Reserve’s Role and Inflation

The Federal Reserve (and other central banks globally) plays a pivotal role. Their decisions on the federal funds rate directly impact the cost of borrowing for lenders, which in turn influences mortgage rates. If inflation continues to moderate and falls closer to the Fed’s target of 2%, there’s a higher probability that the Fed might consider easing its monetary policy, potentially leading to lower interest rates. However, if inflation proves more stubborn, or if unexpected economic shocks occur, the Fed might be forced to keep rates higher for longer, or even consider further hikes.

Economic Growth and Employment

A robust economy with strong job growth typically translates to higher demand for housing. However, sustained economic growth can also fuel inflation, potentially leading to higher rates. Conversely, a slowdown or recession could prompt central banks to lower rates to stimulate economic activity, but this would also be accompanied by job losses and reduced consumer confidence, dampening housing demand. The sweet spot for lower mortgage rates often involves stable, moderate economic growth with controlled inflation.

Geopolitical Factors and Global Markets

It’s also important not to underestimate the impact of geopolitical events and global economic conditions. International conflicts, supply chain disruptions, or significant economic shifts in major global economies can create uncertainty, influencing bond yields (which mortgage rates often track) and investor sentiment. In a world increasingly interconnected, these external factors can have a surprisingly direct impact on local housing markets.

Given these considerations, a likely scenario for 2026 suggests that mortgage rates might stabilize, potentially oscillating within a more predictable range compared to the volatility seen in recent years. While a return to the ultra-low rates of the pandemic era seems unlikely without a significant economic downturn, a gradual downtrend from peak rates is plausible if inflation is brought under control and economic growth remains steady but not overheating. Experts generally anticipate rates to be in the mid-to-high single digits, but the exact figure will depend heavily on the trajectory of inflation and the Fed’s response.

Affordability Challenges in the 2026 Housing Market

Even with potential stabilization or slight decreases in mortgage rates, affordability is expected to remain a significant hurdle for many prospective buyers in the 2026 housing market. The confluence of elevated home prices, higher interest rates compared to pre-pandemic levels, and stagnant wage growth in real terms has squeezed many out of the market.

High Home Prices: A Lingering Legacy

While price growth has slowed, and some markets have seen minor corrections, the overall median home price across many regions remains substantially higher than just a few years ago. This appreciation has created a significant barrier to entry, particularly for first-time buyers who haven’t benefited from previous home equity gains. Even if mortgage rates dip, the sheer size of the loan required to purchase a home at current price levels can still result in unmanageable monthly payments.

The Income-to-Price Ratio

The crucial metric of housing affordability is often the income-to-price ratio. For many years, this ratio has been widening, meaning home prices are growing faster than average household incomes. This trend is a fundamental challenge that will likely persist into 2026. Unless there is a substantial increase in real wages or a significant correction in home prices (which is not widely anticipated on a national scale), this disparity will continue to make homeownership difficult for a large segment of the population.

The Impact on Different Demographics

Affordability challenges are not uniform. They disproportionately affect younger generations, low-to-middle-income families, and individuals in high-cost-of-living areas. These groups often struggle to save for a down payment, qualify for mortgages, and compete with all-cash buyers or those with substantial equity from previous home sales. The 2026 housing market will likely continue to see these demographic divides, potentially widening the gap between homeowners and renters.

Potential Solutions and Government Intervention

Addressing affordability requires multi-faceted solutions. Government programs offering down payment assistance, first-time buyer incentives, and initiatives to increase housing supply could provide some relief. Local zoning reforms to allow for more diverse housing types (e.g., duplexes, townhouses) and increased construction of affordable housing units are also critical. However, the implementation and effectiveness of these measures vary widely and often take time to yield significant results, meaning their full impact might not be felt universally by 2026.

Supply and Demand Dynamics in 2026

The fundamental laws of supply and demand will continue to dictate the health and direction of the 2026 housing market. Understanding these dynamics is key to anticipating price movements and market conditions.

Persistent Low Inventory

Despite recent upticks, housing inventory remains historically low in many areas. A decade of underbuilding following the 2008 financial crisis, coupled with current homeowners being ‘locked in’ by low mortgage rates they secured years ago, means fewer homes are coming onto the market. This structural shortage is a persistent problem and is unlikely to be fully resolved by 2026. New construction, while increasing, still struggles to keep pace with demand, especially given rising material and labor costs.

Demographic Shifts and Buyer Demand

Millennials, the largest generation, are still in their prime home-buying years. As they age and form families, their desire for homeownership will continue to fuel demand. Gen Z is also starting to enter the market, albeit at a slower pace due to affordability constraints. This demographic tailwind suggests that underlying demand for housing will remain robust, even if economic conditions fluctuate. The sheer number of potential buyers will continue to put upward pressure on prices, particularly in desirable locations.

Investor Activity and Second Homes

Investor activity, while having cooled from its peak, still plays a role. Large institutional investors and individual landlords continue to purchase properties, particularly in rental markets, which can reduce the number of homes available for owner-occupants. The market for second homes and vacation properties also contributes to demand, though this segment is often more sensitive to economic downturns and interest rate changes.

The delicate balance between persistently low inventory and sustained demographic-driven demand means that the 2026 housing market is unlikely to experience a widespread crash. Instead, it’s more probable that we will see a continuation of localized market variations, with some areas experiencing modest price gains, others remaining flat, and a few potentially seeing minor corrections, all within the context of constrained supply.

Regional Variations and Hotspots in 2026

It’s crucial to remember that there is no single ‘national’ housing market. The 2026 housing market will be characterized by significant regional variations, influenced by local economic conditions, population growth, and housing policies.

Growth Markets vs. Stagnant Markets

Areas experiencing strong job growth, particularly in high-tech or emerging industries, are likely to continue seeing robust housing demand and potentially higher price appreciation. Cities with diversified economies and attractive quality of life will also remain competitive. Conversely, regions with declining populations, struggling industries, or an oversupply of housing (though rare nationally) might experience slower growth or even slight price declines.

Sun Belt vs. Coastal Cities

The trend of migration to the Sun Belt states (e.g., Florida, Texas, Arizona) is expected to continue, driven by lower costs of living, favorable tax policies, and warmer climates. These areas may continue to see strong demand, though some of the most overheated markets might experience a cooling period as supply catches up and affordability becomes more stretched. Traditional coastal hubs (e.g., California, New York) will likely remain expensive, with demand driven by high-paying jobs, but perhaps with slower appreciation rates compared to the pandemic boom.

Suburbs and Rural Areas

The post-pandemic shift to remote work initially boosted demand in suburban and even rural areas. While some companies are calling employees back to the office, a hybrid work model seems to be here to stay for many. This could sustain demand in areas further afield from urban centers, particularly if they offer better affordability and quality of life. However, markets heavily reliant on purely remote workers might see some moderation if job markets become more centralized again.

For buyers and sellers in 2026, understanding these regional nuances will be paramount. What might be a buyer’s market in one city could remain a seller’s market just a few hundred miles away. Local economic reports, demographic data, and expert analysis will be invaluable resources for navigating these diverse conditions.

The Role of Technology and Innovation

Technology continues to reshape the real estate industry, and its impact will only deepen in the 2026 housing market.

AI and Data Analytics

Artificial intelligence and advanced data analytics are becoming increasingly sophisticated, offering more accurate property valuations, personalized recommendations for buyers, and predictive insights into market trends. These tools can help both consumers and real estate professionals make more informed decisions, potentially streamlining the buying and selling process.

Virtual Reality and Augmented Reality

Virtual and augmented reality tours are already common, but by 2026, they could become even more immersive and detailed. This technology allows buyers to explore properties remotely with unprecedented realism, potentially expanding the geographic reach of buyers and reducing the need for multiple physical showings, especially for out-of-state or international purchasers.

Blockchain and Smart Contracts

While still in nascent stages, blockchain technology has the potential to revolutionize real estate transactions by creating secure, transparent, and immutable records. Smart contracts, executed on a blockchain, could automate parts of the buying and selling process, reducing paperwork, costs, and the time required to close a deal. By 2026, we might see initial adoption of these technologies in niche markets or for specific types of transactions, paving the way for broader integration.

PropTech Innovations

The broader ‘PropTech’ (property technology) sector is constantly innovating, bringing new solutions for property management, financing, and investment. These innovations could help address some of the existing inefficiencies and pain points in the housing market, potentially leading to a more streamlined and transparent experience for all participants in 2026 and beyond.

Advice for Buyers, Sellers, and Investors in 2026

Navigating the 2026 housing market will require strategic planning and adaptability. Here’s tailored advice for different market participants:

- Prioritize Financial Health: Strengthen your credit score, pay down debt, and build a substantial emergency fund. This will put you in a stronger position for mortgage approval and unexpected homeownership costs.

- Save Aggressively for a Down Payment: Even with potential rate shifts, a larger down payment can significantly reduce your monthly mortgage payments and overall interest paid.

- Get Pre-Approved: Understand exactly how much you can afford and what your monthly payments will look like. This also signals to sellers that you are a serious and qualified buyer.

- Be Flexible: Consider alternative housing types (condos, townhouses) or expanding your search to slightly less competitive neighborhoods or even nearby towns if affordability is a major concern.

- Educate Yourself: Stay informed about local market conditions, interest rate forecasts, and government assistance programs. Work with a knowledgeable real estate agent who specializes in your desired area.

For Current Homeowners and Sellers:

- Assess Your Equity: If you’ve been in your home for several years, you likely have significant equity. Understand how much you’ve built and how it can be leveraged for your next move.

- Time Your Sale Strategically: While the market might not be as frenzied as in 2021-2022, well-maintained and appropriately priced homes will still attract buyers. Consult with a local agent to understand the best time to list in your specific area.

- Invest in Key Upgrades: Focus on upgrades that offer a good return on investment, such as kitchen and bathroom renovations, energy-efficient improvements, and curb appeal enhancements.

- Be Realistic on Pricing: The days of multiple over-asking offers might be less common. Price your home competitively based on current market comparables to attract serious buyers.

- Consider Refinancing: If mortgage rates dip significantly in 2026, evaluate if refinancing makes sense for your financial situation.

For Real Estate Investors:

- Focus on Cash Flow: In a potentially higher-rate environment, properties that generate strong rental income will be key. Research rental demand and occupancy rates in target areas.

- Diversify Your Portfolio: Don’t put all your eggs in one basket. Consider different property types (residential, commercial, multi-family) and geographic locations.

- Look for Value-Add Opportunities: Properties that can be improved through renovation or strategic management can offer higher returns even in a more challenging market.

- Understand Local Regulations: Be aware of evolving landlord-tenant laws, zoning changes, and rent control measures in your investment areas.

- Long-Term Perspective: Real estate is generally a long-term investment. While short-term fluctuations are inevitable, focus on the long-term appreciation potential and income generation.

Conclusion: A Cautiously Optimistic Outlook for the 2026 Housing Market

The 2026 housing market is poised to be a period of continued adjustment and normalization, rather than dramatic swings. While a return to the explosive growth of the pandemic years is unlikely, a widespread crash also appears improbable due to persistent underlying demand and structural supply shortages. Mortgage rates are expected to stabilize, potentially with some downward movement if inflation is successfully managed, but they will likely remain higher than the historical lows many have grown accustomed to.

Affordability will continue to be a central challenge, especially for first-time buyers and in high-cost regions. However, regional variations will be significant, offering different opportunities and challenges across the country. Technology will play an increasingly vital role in streamlining transactions and providing market insights.

For all participants, the key to success in the 2026 housing market will be informed decision-making, financial preparedness, and a willingness to adapt to evolving conditions. While the path ahead may not be entirely smooth, a clear understanding of these trends can help individuals and families navigate the complexities and achieve their housing goals.